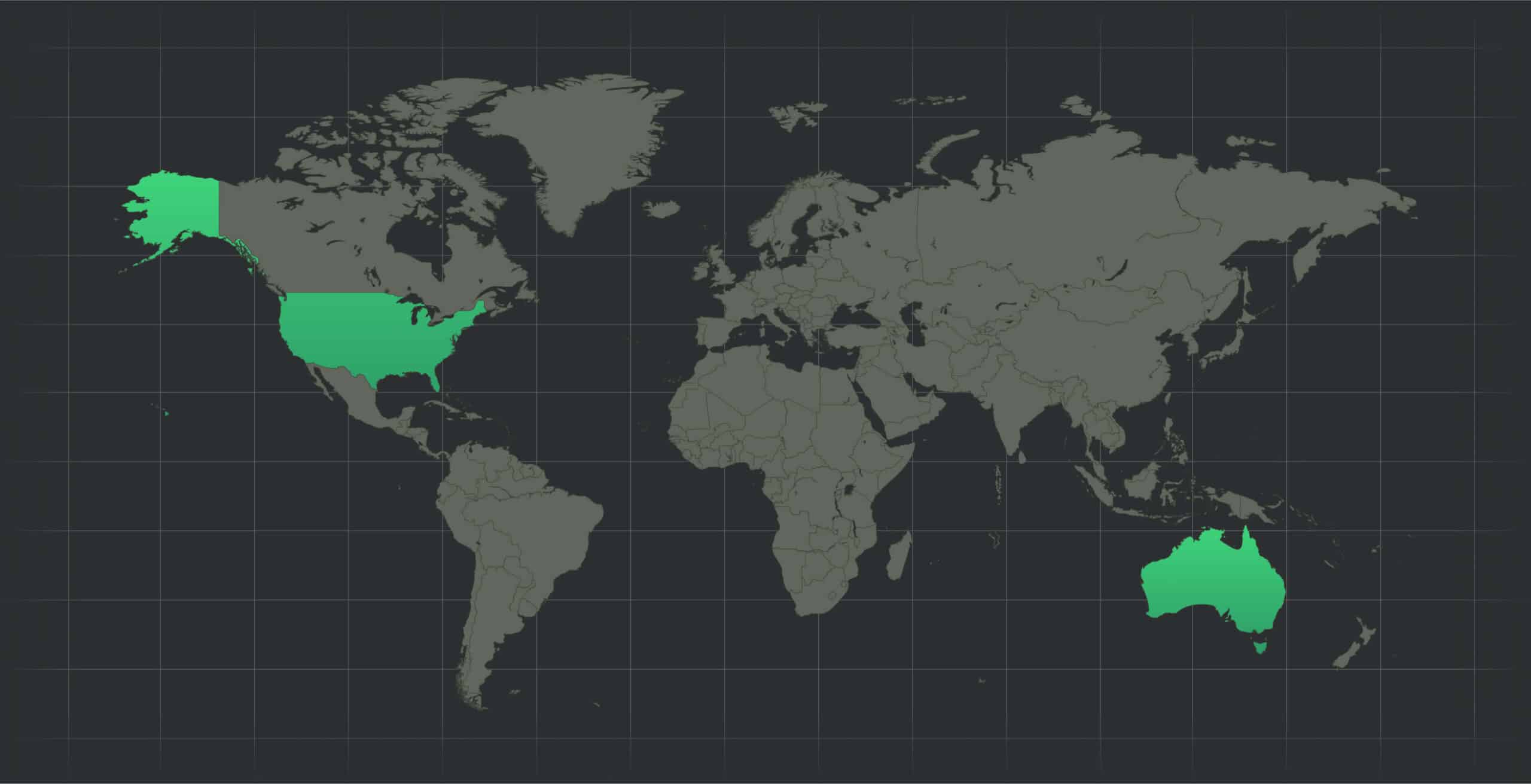

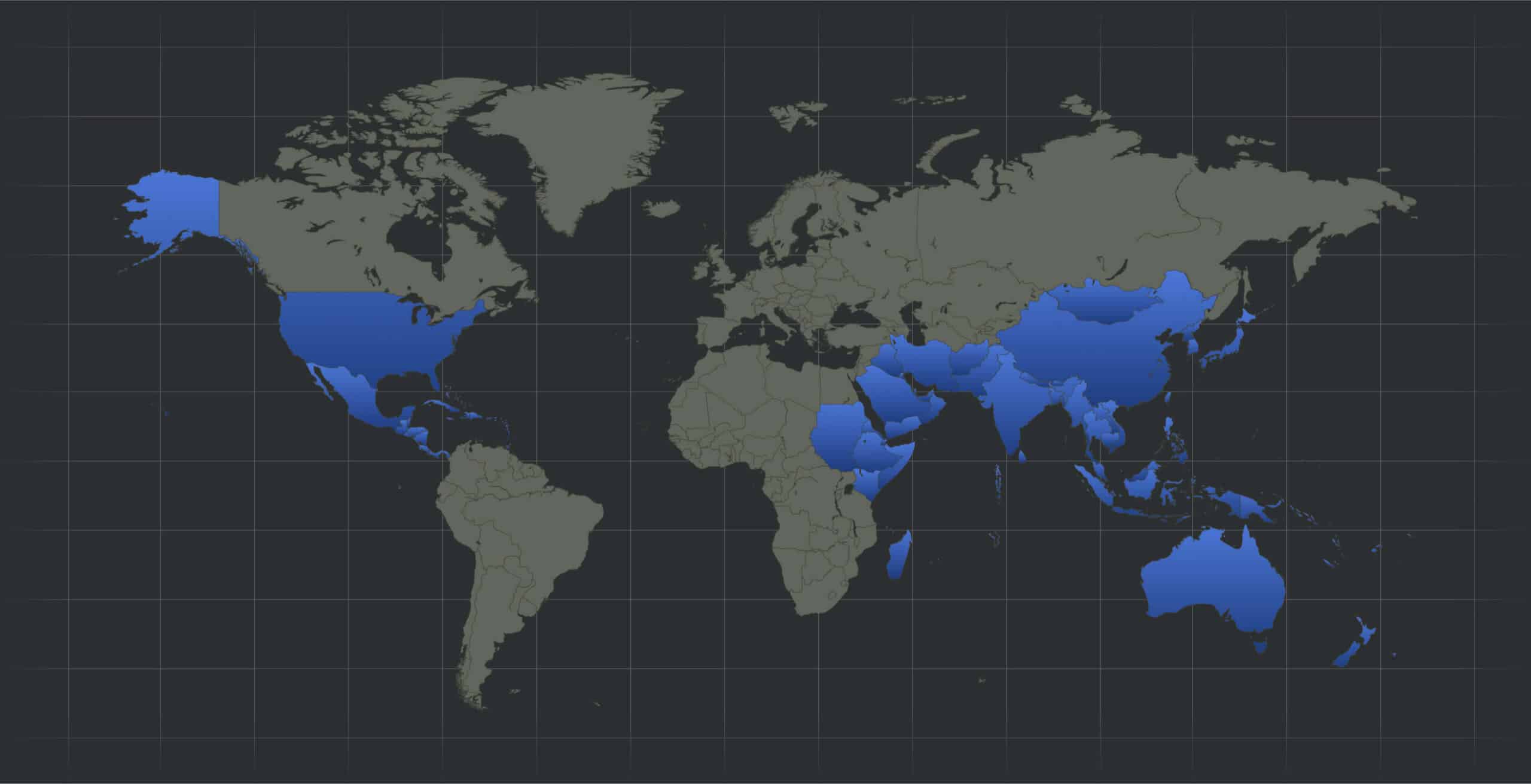

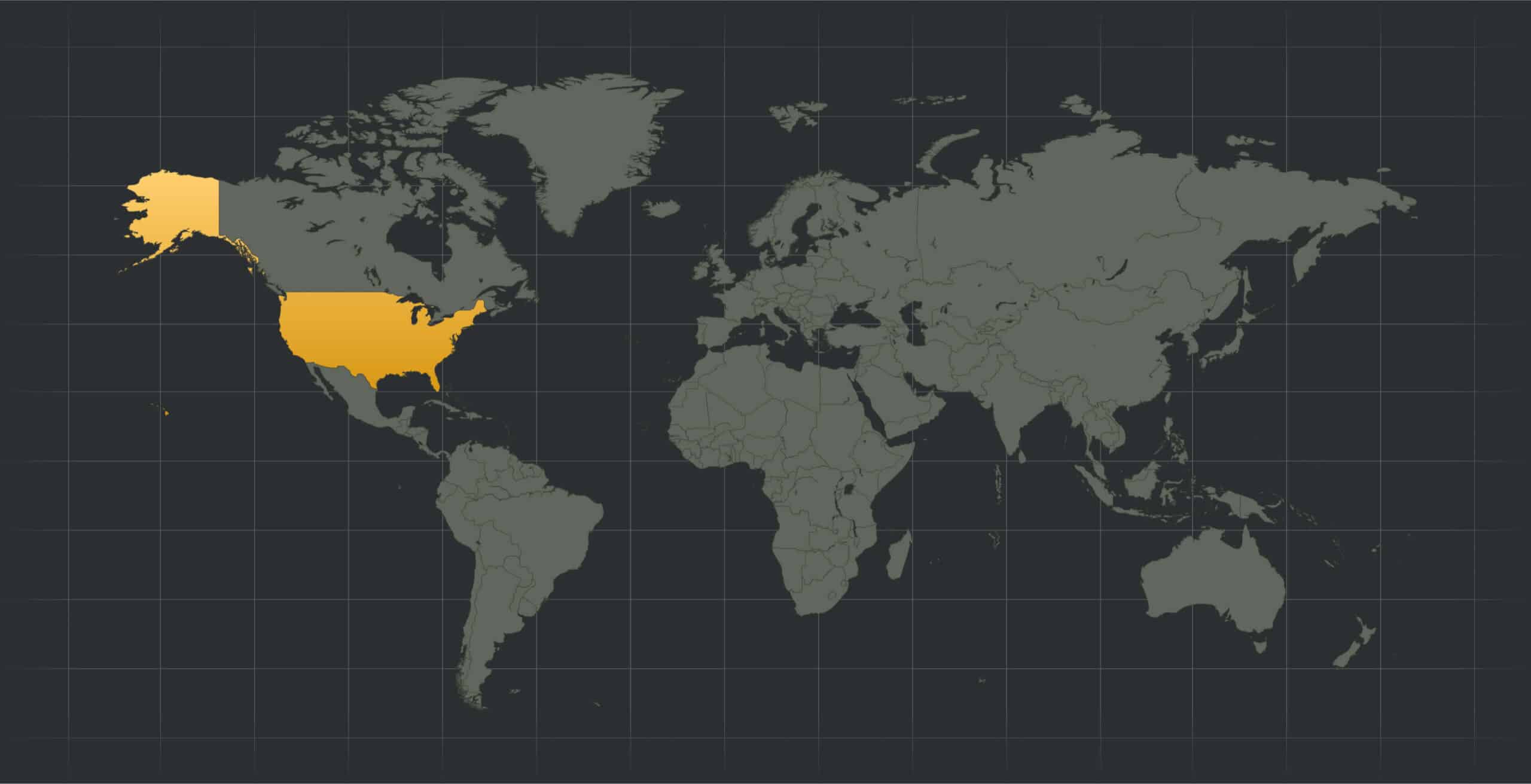

US, Canada, Mexico, Central America, Caribbean, Europe, Australia, New Zealand

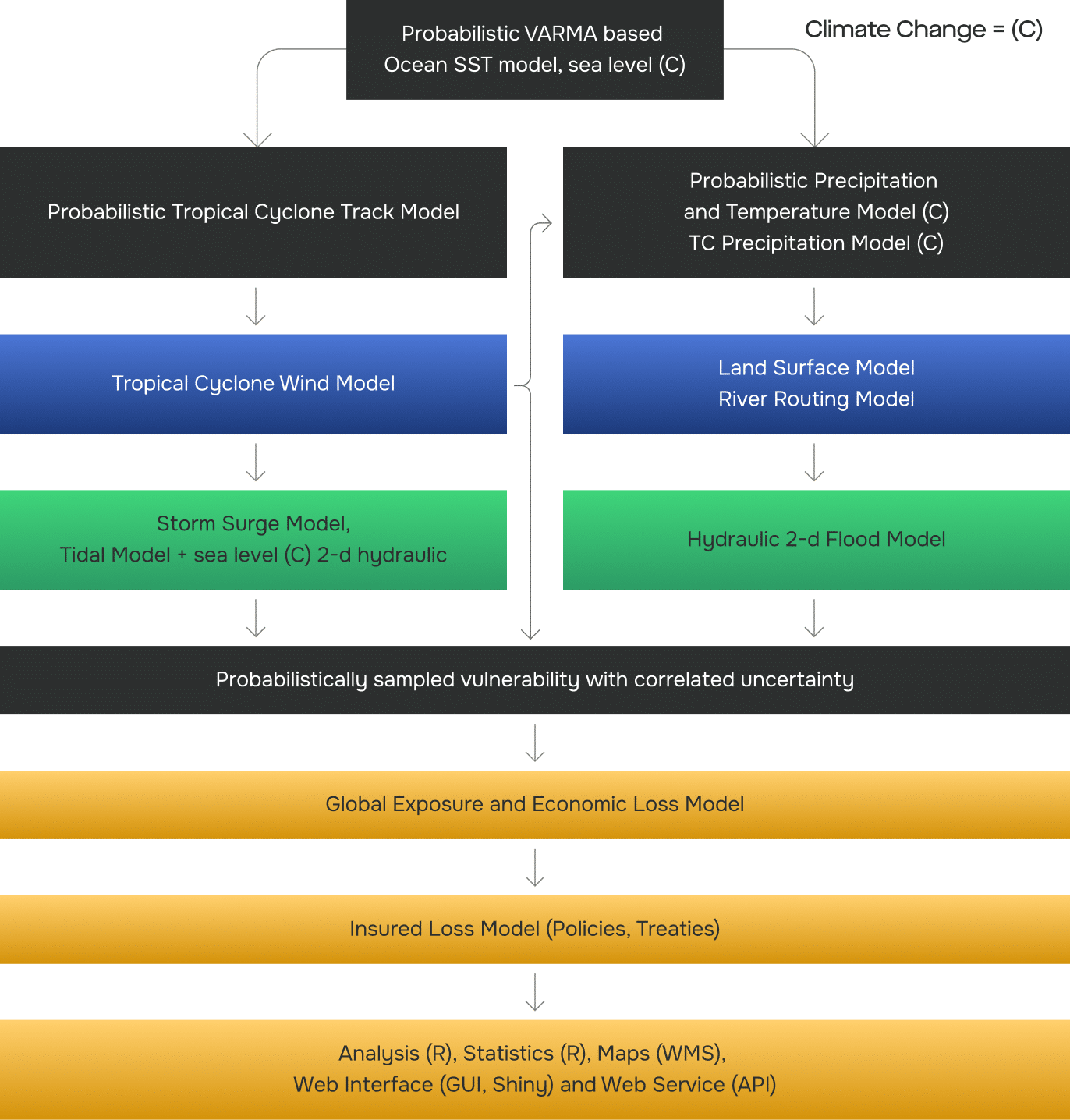

Event sets consist of 50,000 years of simulation and incorporate climate variability.

SpatialKat incorporates fully modifiable vulnerability curves and associated assumptions.

Developed in collaboration with leading global carriers, our financial model is capable of modeling complex insurance structures.

KatRisk models are capable of quantifying the loss impacts of future climate change at the portfolio and location level.

SpatialKat’s event analysis options allow users to understand the potential impacts of critical events on their portfolios before and after the storm.

Catastrophic events are globally correlated with sea surface temperature (SST) as the main driver. We can establish this through linking teleconnections to large scale droughts and floods.